Plummeting prices forced oil and gas companies to get serious about rising production costs. They have. Now the challenge is to preserve those gains.

Since the downturn, production costs and operational losses are down sharply—but can it last?

The fall in oil prices has driven oil and gas companies around the world to focus on reducing production costs. In this article, the first of a regular series providing our perspective on upstream oil and gas operations, we look at global trends in production costs, and how at the same time the reliability and safety of assets have improved. We will use a recent analysis from the UK North Sea to understand the changes and assess their sustainability, along with the key internal and external factors that influence them. The upcoming series will draw from public and proprietary data sources, and recent interviews with senior executives representing both operators and contractors.

Improvements drive costs down as the industry responds to the downturn

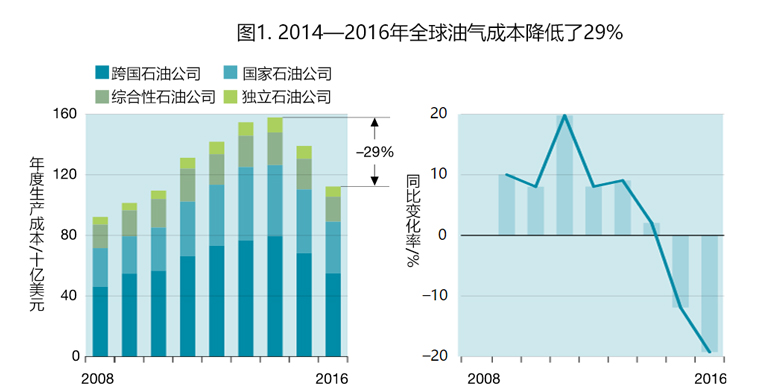

Over the last two-and-a-half years, oil prices have fallen from more than $100 per barrel to less than $35 per barrel, before a recent recovery pushed them back up to $50 per barrel. This drop has been reflected in company spending. While our quarterly perspective on oil field services and equipment1 provided detailed commentary and insight on the 45 percent reduction in global capex spend since 2013, here, for the first time, we perform the same analysis for global production cost, examining the reported cost for a group of 37 oil and gas companies producing close to 40 million barrels per day (Exhibit 1).

Overall, production cost has fallen by an estimated $44 billion (29 percent) since 2014, in contrast to the steeply rising costs we saw in the previous years. For example, between 2008 and 2014, $60 billion was added to production costs for the operators examined. The recent reduction in production cost brings the 2016 operating expenditure back to the level last seen in 2010.

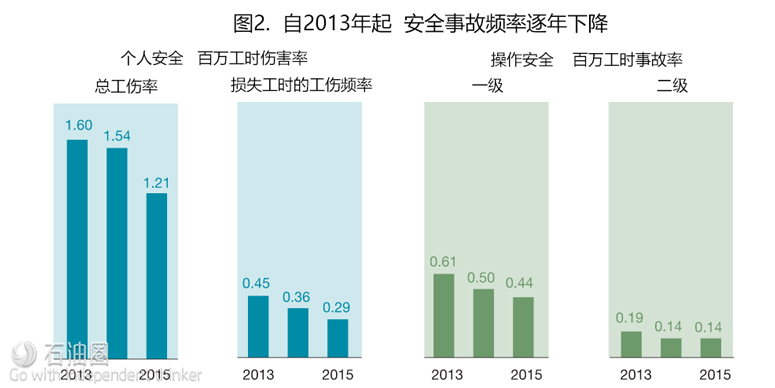

Production cost performance was not the only notable improvement in recent years. International Association of Oil & Gas Producers (IOGP) reports that global safety performance also improved between 2012 and 2015 (the latest year with available data)2 (Exhibit 2).

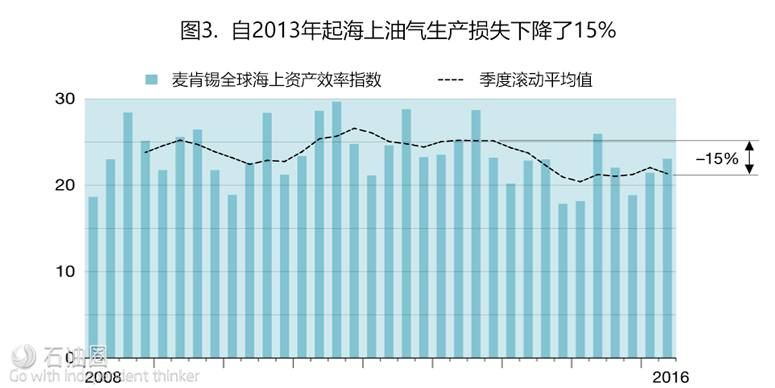

The third area where the industry improved is aggregate operational production losses incurred on producing fields—McKinsey’s new Global Offshore Asset Efficiency index shows a 15 percent reduction in overall losses based on analysis of production data from over 400 offshore installations from the Gulf of Mexico, Brazil, Norway, the United Kingdom, and Thailand producing over 10 million barrels of oil equivalent daily (Exhibit 3). Most of the fall in losses came from a reduction in unplanned outages, but also over 25 percent fewer days across the industry on planned shutdowns as operators reduced the frequency of these events, and scope of work covered.

Are the reductions in production cost sustainable?

Operators have reduced spend in many ways, including realigning their operations and organization through portfolio management, increasing efficiency, and capturing lower prices from goods and services providers due to current market conditions.

To determine if the industry can sustain the current level of production cost, we need to look at the source of cost savings in detail and judge if the savings are temporary, or potentially permanent. Savings from postponing activity are temporary, while savings from lower prices for goods and services are largely dependent upon oil price and market conditions. Eliminated demand and specification changes, however, have the potential to be permanent and sustainable.

We also need to understand what other factors might drive spending higher or lower in the future. For example, an increase in level of activity driven by a higher oil price outlook would affect spending, as would the degree of cooperation between operators and service companies, and technological or regulatory changes.

Insights from cost reduction efforts in the North Sea

We can gain a good insight into these questions by considering the cost reduction efforts made in the UK North Sea since 2014. Oil & Gas UK report that the industry reduced operating cost from £9.7 billion to £7.1 billion (27 percent) from 2014–2016 for a consistent set of fields, while also increasing production efficiency and improving safety performance across the sector.3

In terms of the sources of the savings, our analysis showed that over half came from operational efficiency improvements, and from eliminating unnecessary activities. These reductions have a much greater potential to be sustainable than temporarily deferred activity, or price reductions negotiated on service and equipment (Exhibit 4). We concluded that at least half the savings made should be sustainable even in a higher oil and gas price environment.

The chart categorizes four main types of cost reduction—permanently eliminating planned activity; changes in specification or approach; negotiated supplier price reductions; deferred activity—which are expected to show varying degrees of sustainability. Based on an analysis of over 200 initiatives implemented by operators retrieving over $400 million in operating cost savings between 2015 and 2016, we estimate that 40 to 50 percent of those savings come from the permanent elimination of planned activity, and another 20 to 25 percent comes from changes in specification or approach. Both these types of reductions may be expected either to be sustained, or potentially increased over the next two to three years.

The remaining cost reductions came from negotiating price reductions with suppliers (15 to 20 percent), or from deferring activity (10 to 15 percent). While these last actions are often some of the first initiatives implemented, the resultant reductions are expected to be less sustainable as they are largely dependent on oil price and activity levels. Whether they are preserved is likely to be linked to market conditions rather than factors controlled by operators.

The UK companies we spoke to mentioned two common themes that are relevant beyond the North Sea:

There are more efficiency improvements to be made, but these were judged harder to capture than the reductions achieved so far. Many operators launched efficiency improvement efforts prior to the price fall in Q4 2014. Rising costs in the basin had attracted management attention even before the price collapse. Efforts to reduce those costs—typically programs to identify risk and make improvements across a broad range of activities—increased in pace and intensity with the downturn. The focus for the companies we spoke to has shifted to implementing measures to sustain the efficiency gains made, and to capture additional opportunities.

Many felt there was an opportunity for new, more cooperative ways of working between operators and the supply chain. Supply chain margins in the United Kingdom fell from 10.3 percent to 7.6 percent over this period while supply chain providers saw a 29 percent reduction in revenue, per Oil & Gas UK’s 2016 Economic Report. But at the same time the OGUK Operator Collaboration Index score from April 2016 showed an increase from 5.9 to 6.7 out of a possible 10, suggesting that there has been some recent progress here.

Implications for producers around the world

Simply put, future spending across the world’s oil and gas producing fields will depend on just two things: first, the level of economically viable activity required to maintain existing production and to capture new opportunities at the current prices and, second, the cost of executing that activity, driven by market prices and the efficiency and effectiveness of the industry.

Both these drivers will depend largely on oil price, as that determines what activity is economic, and therefore drives demand on the supply chain. However, spending is also affected by regulatory compliance, technological advances, natural field decline rates, as well as company-specific factors such as the ability to sustain and capture efficiency gains. Nonetheless, our analysis indicated that at least half the savings made to production cost so far should be sustainable even in a higher oil and gas price environment. It will be down to the industry to sustain these gains and push for further efficiency improvements in their cost base. The companies that will succeed use the downturn to learn how to execute activity at a lower cost than previously attainable, by working with the supply chain in new ways, harnessing new technology and refining their operating model.